How to Choose Yourself in Today’s Economy

For years, PayPal has benefited from attracting the world’s entrepreneurs going digital.

For years, PayPal has benefited from attracting the world’s entrepreneurs going digital.

Now, inexplicably, PayPal seems to have decided to intentionally favor that enormous strategic advantage for naive political experiments.

For a very long time, PayPal was the obvious choice for businesses going online.

They supported digital nomads far and wide.

Every year since then, their customer service has been deteriorating, increasingly burdening customers with ridiculous questions and freezing accounts without any due process.

Tried to commission artist in Spain thru PayPal. I had to make a phone call explaining who, what, why, how much, and how many payments there would be in the future. Cancelled. Bitcoin is the future.

— Tshirts4Peace@WhiteRoseTees (@whiterosetees) November 11, 2018

For me personally, travelling while using PayPal is a bit of a hassle.

When you setup a PayPal account in one country, and you travel to another, PayPal is not going to let you login into your account and make a transaction.

To others, PayPal has been labeled a scam, taking their funds for undisclosed reasons.

PayPal, once the envy of the free enterprise market are now asking questions ludicrously irrelevant to their sole function of sending payments.

The payment-service-providers we used to rely on are no longer neutral, borderless and convenient.

This is due to centralization. Our inability to scale socially in a global environment where political prejudice trumps diversity.

Countries that are unbanked, sanctioned or chastised by more powerful countries are ineligible to partake in these financial services.

They’re weapons to punish the poorest and the most vulnerable sections of society.

Take a look at the accounts PayPal have banned and countries that they do not support due to lack of regulation. A total population of around 2 – 3 billion people today.

To do or say nothing and accept the fact is also saying that you can accept the reality of the situation. Of course, until the day no one else can speak up for you.

Only by taking charge of the situation that you can create lasting change.

Hence, I believe everyone should take charge of their own financial well-being. Relying on these so-called “Traditional” financial experiments controlled by a few men in suits is tantamount to suicide.

Instead of using PayPal and giving in to all the red-tape, we should be relying on ourselves for financial security & digital commerce.

I believe that Bitcoin will be the internet of money.

Using Bitcoin also means Choosing Yourself in this digital economy.

While most people consider Bitcoin to be a speculative asset or a get rich quick scheme, there are those at the forefront of this technology consider it to be the future of money.

Unfortunately, at times many don’t understand why and how Bitcoin works.

They assume its slow and expensive because it’s impractical to use Bitcoin to buy coffee or simply wait for 10 – 30 minutes to get confirmation.

They assume it is a get rich quick scheme to make more fiat currency. If you actually took the time to read The Bitcoin Standard, you would laugh at these baseless accusations.

I will try my best to debunk these fallacies today.

The Traditional Banking Business

Bitcoin is a commodity. Lightning is an app that allows you to use this commodity in a currency-like way.

— Nik Bhatia (@timevalueofbtc) November 21, 2018

Building something beautiful takes a lot of hard work and patience.

Just like gardening. You cannot rush it. You must plant well, understand what you’re doing, and pull all weeds up by their root.

Most people want to quickly identify problems in their life and then cut them down. The problem is that, like a weed, they never dig up the root. So, later the same problem comes up. In life and in money, you must understand the root of your problems.

Several years ago, I read a great article that made the case against “Traditional” finance.

In that article, which today rightly identifies, in so many words, that the prosperity that we have long enjoyed is nothing but an illusion portrayed by the ruling class.

Professor Philip Alston, a United Nations Special Rapporteur on extreme poverty and human rights investigated the impact for 8 years in response to the 2008 financial crisis and found evidence of a systematic, willful, concerted and brutal economic war unleashed by the ruling class against its poorest and most vulnerable sections of society.

They also created the myth that our house is an asset. This in part also contributed greatly to our past financial crisis.

I was reminded of that article today, because the current climate haven’t changed much. Society still believes in these same ol’ stories that greed is good and consumerism is the only way we can achieve ever lasting prosperity.

Back in the years following the real estate bubble burst, I learnt a couple of important lessons.

First, inflation creates inequality.

Second, debt controls people.

Third, taxation only benefits the top of the food chain. And fourth, fiat currency is backed by nothing.

To sum up, the dream of becoming wealthy through capitalism is one of the biggest lies ever perpetrated on the public.

In a fiat monetary system, money is created out of thin air. Society believes that greed is good, and everyone else less fortunate can be written-off completely.

The rich will only get richer. This saying no longer does any justice.

According to an Oxfam report, just 8 men own the same wealth as 3.6 Billion people who make up the poorest half of humanity.

From that report we also know that:

- 1 in 10 people survive on less than $2 a day.

- Inequality is trapping hundreds of millions in poverty.

- The first Trillionaire will emerge in 25 years. (Spend $1 million every day for 2738 years to spend $1 Trillion)

- Big Businesses and ultra-wealthy are dodging taxes & lowering wages in order to maximize profit.

- Women working in garment factories in Vietnam work 12 hours/day, 6 days/week @ $1 an hour to produce luxury goods for the world’s biggest brands.

- Winnie Byanyima, the Executive director of Oxfam calls this obscene amounts of wealth in just the hands of a few.

The 0.1% that own half of the world’s wealth have all the islands, yachts, castles and mansions under their names.

There’s a market for the ultra rich simply because of this monopoly.

We pay far too much respect, tribute and worship to the rich and famous, while their main objective is to continue piling up the loot at the top of this elaborate pyramid scheme.

Face it! Capitalism is a dream concocted to blind everyone from exploitation.

Our centralized fiat monetary policy is broken.

It is monopolistic in nature.

Why do ordinary taxpayers need to subsidize the world’s richest people for their own blunder?

Global debt is at an All-Time High of $247 Trillion.

Printing more money will not trickle down into the hands of billions of people.

It only creates an illusion of prosperity.

Unfortunately for many, hindsight is 20/20. And I fear what the future may hold for people treading conventional paths.

Thankfully, Bitcoin was invented.

It is the money for the people by the people.

Read: Bitcoin is a Hedge Against the Stupidity of Politicians

Mass media will always have you believe otherwise.

When people ask me what they should read to understand Bitcoin, I always suggest they start where it all started with the Satoshi Nakamoto white paper which is ten years old today: https://bitcoin.org/bitcoin.pdf

We’re living in the age of power, money and control, where media companies from Instagram to Facebook to the Washington Post or the New York Times are controlled by people with mountains of cash.

They maintain that same control until today because of their ability to move mass public perception.

If you’re not familiar with the history of money, you need to educate yourself. I also got my start this way.

There’s no denying that the centralize monetary policy has been and always will be a problem. But even though banks are a problem, it’s not the real problem.

The real problem is the fundamental lack of financial education. The real problem is that people don’t fundamentally understand how money works.

Policies make it far too complicated for ordinary people to understand completely.

Numbers can easily be tampered with, mass public psychology can be swayed and most people are trapped in a bubble of debt that makes it hard to see their economic situations clearly.

PayPal is Turning into a Bank

PayPal used to be a simple and neutral platform that allows anyone to transfer money using the internet.

Today, that is no longer the case.

They’re quietly partnering smaller banks in an effort to move into traditional banking by offering their user base debit cards, direct deposits and other financial institution services.

Aligned with this underlying motive, PayPal is randomly scrutinizing their customers’ intention and the nature of their funds. They can freeze your account and hold your money for undisclosed reasons.

They call their “Good intentions” benevolent in nature that satisfies their company’s core beliefs.

What’s happening is that PayPal is stepping up political control because they fear their masters, far more than they care about you or me as their customers.

Question is, should these powers be granted the right to control the free flow of money in the first place? Or should the free exchange of money be anyone’s god-given right?

PayPal started as a free enterprise, but they’re gradually leaving all that behind for political gains.

Who is Winning the Race?

BREAKING: 🚨

Bitcoin Transaction Value Reaches $1.3T As It Passes PayPal…

The times are changing 😉 pic.twitter.com/bAMFbO19Bg

— Gold Telegraph (@GoldTelegraph_) September 3, 2018

Speed of Payment

Like email, digits on the internet is just bytes of data that can travel at near instantaneous speeds. But why is moving 💰💰💰 money over the internet so god-darn slow?

Did you know that most of the world’s money resides within the accounts of 26,000 banks across the world?

Therefore, speed would be measured by how fast one payment can move from one bank to another, often times in another country.

We’re talking about borderless transactions over the internet. Domestic payments are fast and cheap, but once money has to cross borders, the speed would slow to a crawl.

The issue with PayPal is that it just facilitates payment on the internet from your bank account to your counterpart’s bank account which will drastically hinder the speed of your transaction.

Wiring money from your bank is whole other story.

Once I made a wiring transfer of just $80 from Singapore to the US.

The bank charged me $50 just to do that. What’s more I had to wait another 5 agonizing days before my payments arrive at the recipient bank.

The problem with banks is, that they will tell you that your international wire will cost a bomb and it will “probably” arrive in 3 – 5 days.

Meaning? it could get lost somewhere in between.

So why does it take so long for your money to move across borders on the internet?

Imagine sending money to Bob over the purchase of his product using PayPal.

I would first need to receive money inside my account from my bank account in my country. If you use your debit or credit card, it would cost you a fee.

Then, PayPal would need to process that, check and convert your local currency to the designated recipient’s currency.

After that, deliver your payment to your recipients bank account in his country.

Where’s the bottle-neck?

Sending money from my bank account to PayPal’s bank account, that’s the slow part.

Paying with your card may be faster, but much more expensive.

Bank transfers are fast in certain countries like the UK, Singapore and Hong Kong. But even if you’re in the Eurozone, Australia, US or Canada, it will still take time to receive that payment.

Sure, you could trust PayPal and park your money inside their account for future payments, question is, do you trust them enough to store your hard earned money with them?

In small amounts, probably. Larger amounts, definitely not.

Fees: Bitcoin’s Too Expensive?

Recently, Binance a cryptocurrency exchange moved its bitcoin worth $600 Million dollars for just a $8 fee.

Yes you heard that right!

Binance just moved half a billion dollars for a fee of 0.00001%. Bitcoin is still magical.https://t.co/RUgZRaUrvs

— Ryan Selkis (@twobitidiot) November 18, 2018

In any other transfer, they would have had to pay $18 Million in fees @3% to move.

What’s so unique & mind-boggling with Bitcoin is that the fees are based upon the amount of computer resources needed to store data. And that transaction of $600 million was just 1550 bytes.

Now, the network capacity also affects the fees, so earlier in December 2017 because of the sudden spike in interest, people were paying an average fee of $28.

Others complain that they had to pay a fee of $16 to send just $25 worth of Bitcoin.

Whatever the fees future participants will have to pay, it’s all about understanding what Bitcoin is.

Bitcoin is like a container ship of value transfer and storage. It’s monetary policy is fixed at 21 million BTC. So it doesn’t really make sense buying a cup of coffee with Bitcoin rather than using fiat money.

Inflation is built into the fiat monetary system. Whereas Bitcoin is deflationary and scarcity will only increase its value over time.

2/ A monetary system is always built in layers, and Bitcoin is meant to be the base most layer, where the most trust in settlement is required.

The Lightning Network, built atop Bitcoin, is like the last-mile delivery service that gets that small package to someone’s doorstep. pic.twitter.com/OCk8xrxzxA

— Vijay Boyapati (@real_vijay) November 1, 2018

What is The Lightning Network?

Lightning is a layer built on top of the Bitcoin blockchain.

It is a solution to solve the scaling problem that existed within Bitcoin.

Because of the decentralized nature of Bitcoin’s blockchain using Proof-of-work, transactions can get be pretty slow when compared to centralized systems like VISA.

With VISA, 25,000 transaction per second is not a problem, but Bitcoin can only handle about 7 transactions per second.

Lightning can handle 50,000 transactions per second.

For much smaller transactions, it doesn’t make much sense to record it on the Bitcoin blockchain, rather it’s much simpler to just setup a payment channel like a wallet where the participants involved can quickly send each other small amounts of bitcoin at infinitesimal fees.

I’m talking about fees at 1 Satoshi per transaction (0.00000001 btc).

So when the participants decide that they want to settle all the balances and close the channel, the final balances are only then recorded to the Bitcoin blockchain.

Essentially, the Lightning Network is generating IOUs between participants and technically no one actually holds real bitcoins within the channel while its open.

Eventually when the last IOU is settled, the channel would then close. After that, the final balances are recorded to the Bitcoin blockchain accordingly.

At the moment, Bitcoin’s Lightning Network has the capacity to handle over $2 million in BTC and has grown by 300% in the last 10 days.

Security

No banking product, PayPal or even the infamous Fort Knox is safer than the security of a cold storage wallet in which you can secure your bitcoins.

A cold storage wallet, one like the Ledger Nano S or the Trezor is not connected to the internet at all times.

Whenever you do connect to the internet, it would require your unique pin number in order to send or receive any transactions.

With good security habits, you can access your own personal fortune at any time without needing banks or even PayPal.

The Bitcoin network itself is tremendously resilient because of its decentralized network architecture.

Highly acclaimed security specialists like Dan Kaminsky tried to hack Bitcoin but ultimately failed.

If you don’t know who he is and the significance of Dan trying to hack Bitcoin, then imagine this…

Try winning the Powerball nine times in a row.

It’s highly unlikely even once right? Well, your odds of striking it not once, not twice, not thrice but nine times gets infinitely worse. And that is still an understatement.

Banks security and PayPal? Bah, for as little as $2, someone could easily gain access to your PayPal account.

and banks? Their technology is archaic, something like Bubble boy. In fact, their web apps are some of the most vulnerable points of security the internet has ever seen. Read the news…

So, don’t count on the safety of our bank account or the complexity of your PayPal password phrase.

Irreversible transactions

What happens if you accidentally sent some stranger your precious bitcoins?

Well, you would lose them forever.

If you send money via PayPal or bought something fraudulent on the internet with your Credit Card, you could still recover the funds back even up to 90 – 180 days.

Which one would you prefer? I bet the latter.

But consider this, reversible transactions never occurred until credit cards were introduced.

A centralized controlling entity have power over the money you use. It can also print more money out of thin air.

Reversing your transactions is easy because it’s just IOUs.

Essentially, we all pay a price for the convenience of having to trust centralized entities .

And that price is paid with the purchasing power of your dollar.

How you treat a dollar today is different from how your father treated a dollar in his time 10 years ago. All this is connected to your time preference.

Watch this 6 minute video explaining why Bitcoin’s irreversible transactions is one of its greatest strengths:

User Experience

Using Bitcoin is undoubtedly more challenging for the average consumer because the technology is still in its infancy.

PayPal on the other hand had a 10 year head-start.

No doubt, PayPal was designed from the get go to solve a very basic problem of transacting money on the internet. That’s the one good thing they could do, it’s intuitive user-interfaces.

Bitcoin on the other hand was envisioned to be a “Traditional Banking” Killer.

As a decentralized monetary system that’s highly secure, neutral, borderless and censorship-resistant, there’s no easy way to design it.

Being permissionless, any Tom, Dick and Harry can spin up a computer/node and verify all the transactions by him/herself. That makes it Tamper-proof.

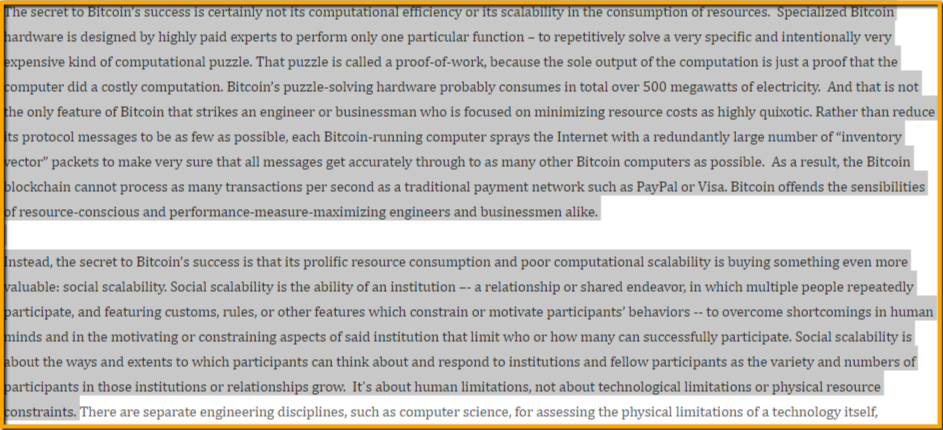

Its network is highly redundant, spraying the internet with thousands of similar packets of data all over the world to achieve one simple thing.

Social scalability.

“Bitcoin offends the sensibilities of the resource-conscious and performance-measure-maximizing engineers and business people alike” ~ Nick Szabo

It’s about human limitations not technological limitations that can be solved in one giant centralized database.

The simplicity of using Bitcoins is progressing over time. As more and more people and billions of dollars come pouring into the ecosystem, we’ll begin to see better and more user friendly features introduced.

At the moment you will already find that some Bitcoin wallets have pretty sleek interfaces like the CashApp by Jack Dorsey, or Ledger Live for your Bitcoin hardware wallet.

Getting a head-start over your peers is definitely a killer move. In no time at all, you’ll be at the frontier of this technology that will change the lives of billions.

Tend Your Garden

Today, you have a choice to do surface work on your garden or to instead get down on your hands and knees, roll up your sleeves, and begin the hard work of tending your financial garden well.

While it will be hard work, it will be work that will pay off for the rest of your life.

By pulling up the roots of your financial problems, you’ll assure they won’t come back in areas and times you least expect.