Did you know that if we could all somehow pay every single penny we have, it would still not be enough to pay off our national debt?

Anyone telling you that you can get out of the debt cycle with just a few simple steps is telling you an outright lie. Today, the global amount of debt in the world has rose to over a quarter of a quadrillion dollars. That’s $247 Trillion as of the first quarter of 2018.

Many still believe we could gradually refinance the mountain of debt we’re in and pay it off over time, but as you can see below that isn’t going to be the case with each passing year as it gets from bad to worse.

“Money is the bubble that never pops” or so they say. Tell the Venezuelans or Zimbabweans that and they’ll scoff at you. Of course debt is the function of any working economy in order to fund spending on a country’s infrastructure or tax cuts, but if left unchecked borrowing can lead to dire consequences especially when there is an economic downturn.

Why Should I care? I’m not in debt.

Whether you like it or not, every man, woman and child will have to pay the price for our out of control spending when the time comes.

Aside from the stark warning issued by the Institute of international finance, the IIF, this has been a growing cause of concern for many developed and developing countries around the world.

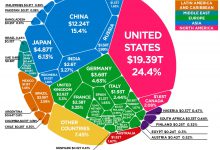

The US for example has a national debt of over $21 trillion and it is growing rapidly. Economic experts have been saying this is unsustainable for the past few years, and yet everyone’s turning a deaf ear. We are going to continue pilling up the pressure on our future finances instead of remedying our ways today.

When It does implode, it will come down extremely hard on everyone…

Bill Gates: It is a ‘certainty’ we will have another financial crisis… Said on Reddit ~ March 2018

If you look at what happens right after a major economic crash, just turn to the Japanese. The Japanese has been battling economic deflation for the past 20 years. Although stagnation in Japan has a lot to do with other socio-economic challenges, a simple look at their public debt to GDP ratio at over 200% would indicate that the US and many other developed countries around the world are in fact stuck in the same cycle of debt.

The Bank of Japan, as of last October, owned 74% of the total volume of the ETFs trading on the Nikkei. Now that number is up to 80%

Printing money to buy assets = monetary fraud… pic.twitter.com/rSXJMOeTRm

— Gold Telegraph (@GoldTelegraph_) July 11, 2018

Overall the US Total debt (National + private debt) is over $70 Trillion dollars. 35 years ago, that number was just 4.3 trillion dollars. So there is no way in hell that all that mountain of debt can ever be repaid in full.

What governments of the world are doing with debt is stimulating the short term economy and continue to enrich its top 1% hierarchy which will end up restricting the future freedom of its citizens at all levels. I won’t go into the details about what a country can do to reduce its debt.

In the end, the effort will always go into increasing our monetary supply. Because its easy, that’s why they call it Quantitative Easing (QE). The process in which they inject money into the economy with newly created electronic-cash.

Trillions of dollars of tax payers money for Bailouts, interests rate hikes, tax hikes or budget cuts… Who suffers in the end? The people down the pecking order. Like an elaborate pyramid scheme.

Most people trade in their time to save their hard-earned money to store it in a bank and hope that one day, it would be enough to buy a home or maybe opt for early retirement.

Unfortunately, it never goes according to plan. Your retirement age raises by the time you get to 60 and you now find out you have to continue working to pay the bills and keep up with your lifestyle.

We are like frogs in a pot of water with the Feds slowly raising the heat on us.

Ever since the Feds was established in 1913, the dollar has shrunk in value to just $0.05 in 2013. Imagine how much it would be worth then in a couple of more decades…

Worst still is that most people are unaware that the US debt is far larger than the total amount of money in their bank accounts. When they think about money, they’d usually think about all the coins, paper money in their checking accounts. But all of that currency is just considered as the M1 money supply.

A measure of the money supply that includes all physical money, such as coins and currency, as well as demand deposits, checking accounts and Negotiable Order of Withdrawal (NOW) accounts. M1 measures the most liquid components of the money supply, as it contains cash and assets that can quickly be converted to currency.

From the chart below, M1 can be seen growing in large quantities in recent years thanks in part of rampant quantitative easing by the Federal Reserve. Even so as of 2015, all of M1 is sitting around 3 trillion dollars…

So imagine you’ve accumulated up all coins, all the paper currency and all money in everyone’s checking accounts, could we even make a dent in all that debt we’ve incurred?

The answer is naught.

So where can we find more money?

Well, there’s of course M2 and M3 money supply. Near money and near, near money, created out of thin air from “1s” and “0s”. All of that additional money supply from large time deposits to market funds just constitutes an estimate of another $30 Trillion dollars.

So even with all that ones and zeroes, it would still be impossible to even pay off half of the US Total debt. And this figure is just getting bigger and bigger each year.

Sure the US is still very rich, investors are still confident, debts get forgotten; as long as the US keeps it up, it should be fine right? Question is, how long can they keep it up with an already overblown budget.

Expending effort creating money, granted it costs less than the actual value of the money itself, makes all the sense in the world. The money medium has value so getting more of it for less than its value is a no-brainer. What’s more, these don’t actually add to the productive capacity of an economy. Adding to the supply of money doesn’t actually help anything, just redistributes the wealth to those creating more of the supply from those that save.

Make no mistake, things are already in a huge mess and yet we are being told they’re under control.

Our current centralized monetary system has been dying a very slow death. It’s running out of steam.

As the rich gets richer, the middle class gets wiped out and the poor, well remains as such.

Any responsible entity, let alone a person who’s run deep in debt would first need to realize that the real problem here is our out of control spending.

For nations to get out of this debt cycle, they must understand that a debt-fueled bubble does not go on forever, it has a limited lifespan.

Someday this bubble is going to burst and then we’re going to live to regret it.

It is just a matter of time.

Inflation Creates a High Time Preference Society that continues to lead us in a downward Spiral…

A high time preference person is short term minded. Prefers Instant gratification. They want to make quick gains, profit now, spend now, do anything or everything as soon as possible.

A low time preference person prefers delayed gratification, because they know their efforts and hard work today would bear fruit tomorrow. Just willing to wait longer than most people would do wonders to his/her own economic need in the future. They understand by forgoing certain pleasures now, could mean something much much better for themselves in the future.

Society’s self-destructive addiction to faster living stems from a very simple fact. A desire to keep up with everyone else. With Social Media platforms like Facebook and Instagram, keeping up with the Joneses has become a chronic lifestyle choice.

Today we’re caught in a chaotic, frenzied spiral of this new addiction, people are chasing money, power, success at a wilder, faster pace of life.

Everybody tend to believe this is the new norm, although everything is spiraling out of control; their behavior, feelings and thoughts.

A nation full of high time preference people will not think much about their future. Instead of sowing the seeds for tomorrow, they would prefer to consume now and bear with the consequences later on. A nation full of high time preference people would be highly unproductive and dependent on the state.

For nations to continue sustaining towards the future, we will need to plan ahead, think long-term. And that requires lots of people who have a low time preference.

According to Saifedean Ammous, a Professor of Economics in the US, “Our monetary policy affects the time preference of a population…”, with an ever decreasing purchasing power, people tend to spend now, rather than save for later attitude.

You can imagine countries that are experiencing hyperinflation to have a very high time preference, because the money they save in their bank would diminish in value very quickly. That’s why they would rather spend their money as quickly as possible.

Countries such as Venezuela, are dealing with the consequences right now. A cup of coffee would cost in upwards of 1 million Bolivars (VEF). And a family of four would need 545 million VEF just for basic goods and services.

There in Venezuela, Bitcoin isn’t a Game, it is an iron-clad monetary policy. Supply is hard-coded and capped at 21 million coins.

For them, Bitcoin safeguards their monetary value and protects them from the highly incompetent political leaders, greedy and corrupt individuals who enrich their self at the expense of the country’s economy.

Bitcoin is insurance against politicians. It protects us from ourselves. Unless of course your leaders are selfless, highly competent, honest and not corrupt. A very rare breed indeed…

The entire banking industry? Well, a large part of it is creating money out of thin air. They call it investing. But does it really add productivity and value to the entire ecosystem? One thing is for sure, they’re lining up their own pockets very well.

These are things that many people understand very little of, and when there is an economic crisis, you and me the taxpayers have to bail them out???

Are you sure the money in your Bank is Yours?

The very first modern central bank was founded in Amsterdam in 1609. Then In the early 17th Century, a war between Serbian separatist and Austro-Hungarians emptied the coffers of the nations involved.

Central banks then spawned throughout the world, establishing in many European countries. Many notable ones included the likes of the Bank of England.

Kings and leaders of nations then used their control of the public’s money to wage war and colonize other countries. They had found the perfect way to improve the public financing of warfare.

In those days, the value of the coin was purely backed by the value of the metal contained within. So countries with vast Gold deposits were extremely wealthy. That’s why countries like Spain, England and Portugal were sending armadas across the globe. They were in search of more gold.

As the gold standard was adopted by the mid-1800, governments guaranteed that they would redeem any amount of paper money for its value in gold. Trade no longer had to be done with heavy gold coins or bullion.

Problem is, prices of gold drops everytime miners found new gold deposits. Read more history of the Gold Standard here.

Fiat money was introduced by central banks as a way of taking control of their public’s monetary value. War and the depression caused the Gold Standard to be suspended several times until finally Franklin Roosevelt secretly ended the Gold Standard once and for all.

Not only that, governments could now eliminate “enemies of the state“, people they do not approve of simply by confiscating their bank accounts. Easy! Governments had more control over their people more than ever in its history.

Be a good citizen, or else!

Although governments and leaders in power hold their people accountable for their crimes, they rarely ever hold themselves accountable. Government corruption has been more rampant than ever across the world.

Perhaps less governance in monetary policies would be ideal?

Read more at 11 Pieces of Bad Advice I Wish People Would Stop Spreading about Bitcoin

A Movement to Regain Control of Our Money

After the global financial crisis of 2007-2008, an anonymous programmer or a group of Cyperpunks found a solution to creating a decentralized network that no one had complete control.

Bitcoin.

It is incorruptible precisely because it is designed and programmed to operate with the least amount of human intervention.

What’s vastly different about Bitcoin’s monetary policy is there is no puppet master or ring leader making any decisions behind any closed doors.

No one could ever seize your Bitcoin or hack into your account because you keep your own private keys. Whats-more, you can memorize your passphrases inside your head and carry your savings across countries.

Read more How to Buy Bitcoin In Different Countries [+International Infographic Guide].

Conclusion

Fiat money is generally inappropriate for the majority of us who aren’t Warren Buffett’s or Wall Street Investors.

It isn’t a good store of value nor is it Sound money.

It incentives those in power to want to keep the status quo. And that means fat corrupted leaders, cronyism, wastage, malinvestments and unskilled money investors.

Bitcoin brings back sound money and therefore promotes sound planning for our future. And that changes everything.

It steers the rudder of the ship back in the right direction.

We haven’t arrive yet, but Bitcoin’s Open, Decentralized Blockchain Network promotes this value proposition.

Like this article? Save it to Pinterest!

Related articles:

- Why Crypto matters MORE For Digital Nomads in 2018

- 11 Pieces of Bad Advice I Wish People Would Stop Spreading about Bitcoin

- Is it safe to invest in Bitcoin now?

- How to Buy Bitcoin In Different Countries [+International Infographic Guide]

- The Cryptocurrency Arms Race

- What is Decentralization and Why it Matters Today

- Buy Bitcoin With Paypal Instantly on these sites (Explained Step-by-step)